I am struck by how different instructors use various parts of our system to teach essentially the same thing. In fact, when someone asks how to teach something using our system, the answer mostly depends on your style of teaching. This is hard to explain in the abstract, so let me give you an example. on teaching Bond Valuation. A previous post shows you alternative ways to teach portfolio diversification.

The basics of teaching bond valuation include understanding discounting and the price-yield relationship, the term structure of interest rates, spot and forward rates, and perhaps managing interest rate risk using duration and convexity. These topics are taught in at least 3 different ways:

Method 1: Bond Tutor - This is an interactive textbook; calculators are embedded into the online text, and students can experiment with concepts as they learn about them. For example, students can change the yield curve or forward curve, and observe the effect on the other curve and also on bond values:

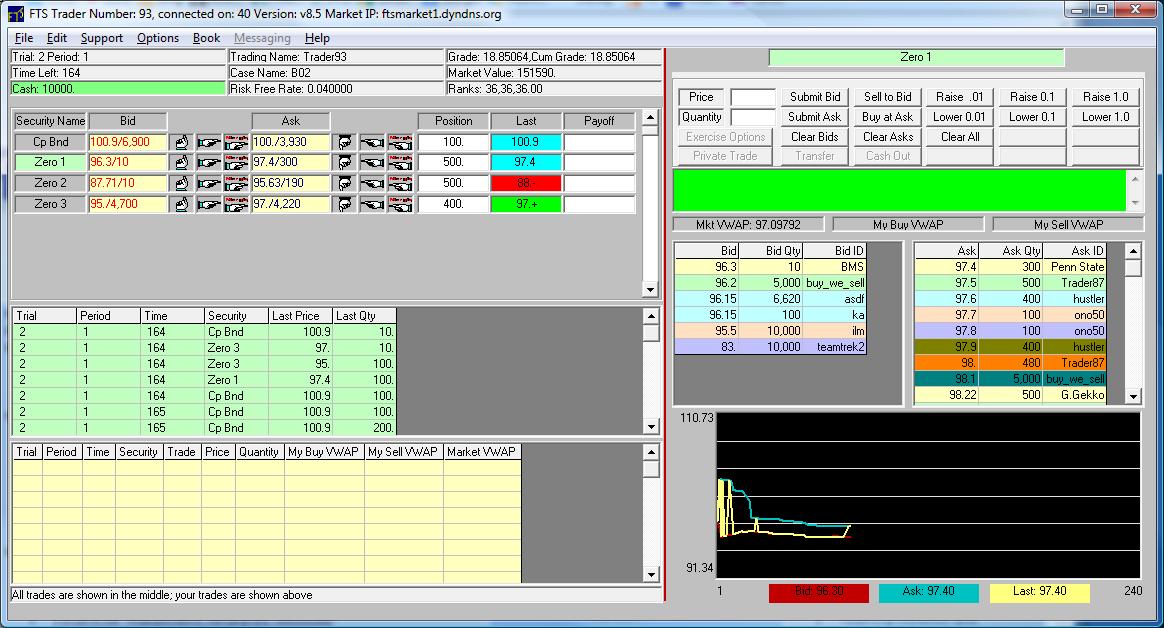

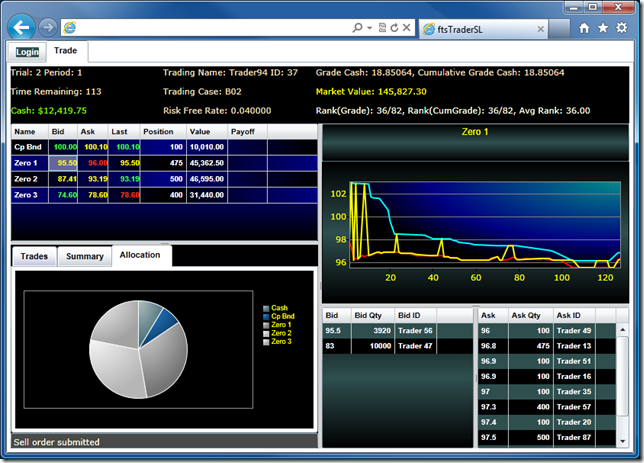

Method 2: The FTS Interactive Markets- Here, students trade bonds and learning takes place through price discovery and by building an analytical support system to help their trading. In the simplest case (B01), there is a flat yield curve, so you learn how to discount given a yield. Students who do not discount correctly lose money in the trading exercise to others. Cases B02 and B03 introduce spot rates and forward rates. Case B04 requires them to hedge a bond portfolio using duration. Subsequent cases build on this, and the most advanced have trading of swaps as well as caps and floors to manage interest rate risk. This is a synchronous “in class” exercise; students trade with each other, they react to each other. Learning goes beyond a textbook; you need to understand the concepts, but you also learn how to use the concepts in making a trading decision. The biggest way in which they lear is by building a decision support system in Excel. The Student Case Preparation Manual shows you what students have to do to prepare for the case and how the learning takes place. The following screen shows a real example of the FTS Interactive Trader with trading case B02:

{kind=link}

You can see my position in two bonds, and importantly, the portfolio analytics at the bottom right, and these analytics are used by students to make trading decisions.

Summary These methods are not exclusive, and my description of what is available is not exhaustive (see below). Bond Tutor represents the smallest deviation from a traditional textbook. The FTS Interactive Markets are short trading exercises and it is easy to introduce the trading exercise in class and conduct a discussion that relates the concept to the trading exercise and also to markets and price discovery. The FTS Real Time exercise abstracts away from price discovery but exposes students to application of the concepts to real-world interest rate movements.

Just as an aside, we have several other modules for teaching fixed income; these include:

--The Treasury Calculator (the relationship between quoted Treasury prices and yields; yield curve approximations and interpolation; understand duration and convexity)

-- The Bond Immunization Lesson (a self contained interactive lesson for understanding how immunization works)

-- The Interest Rate Risk Module (Plot historical yields, spot rates, and forward rates, Animate curves to get a visual feel for long terms trends and mean reversion, Calculate volatilities and correlations, Conduct principal component analysis, Backtest to understand the efficacy of different immunization strategies)

--The Principal Components Lesson (Understand the essence of principal component analysis with a visual calculator)

--The BDT (Black-Derman-Toy) Module (calibrate a BDT model to your own yield curve data using either yield volatilities or local vitalities, transfer the calculated lattice to Excel to price interest rate derivatives)